Each year, our State of Subscription Apps report sets out to understand what’s changing in the industry; what’s new, what’s over, and what’s on its way. This year, our dataset grew again: over 115,000 apps, representing more than $16 billion in revenue. And we analyzed the data from all 115k+ of them.

If you thought last year’s report was a behemoth, look away now. This year, we’ve delivered 338 pages, ready to give you every metric, benchmark, or trend you could possibly need.

To summarize David Barnard’s own words, “There’s a lot of apps making a lot of money.”

But, if you (shockingly) don’t have time to read every single page (like David and Jacob did), then this rundown’s for you. Strap in.

1. Subscription app growth is no longer a spectrum

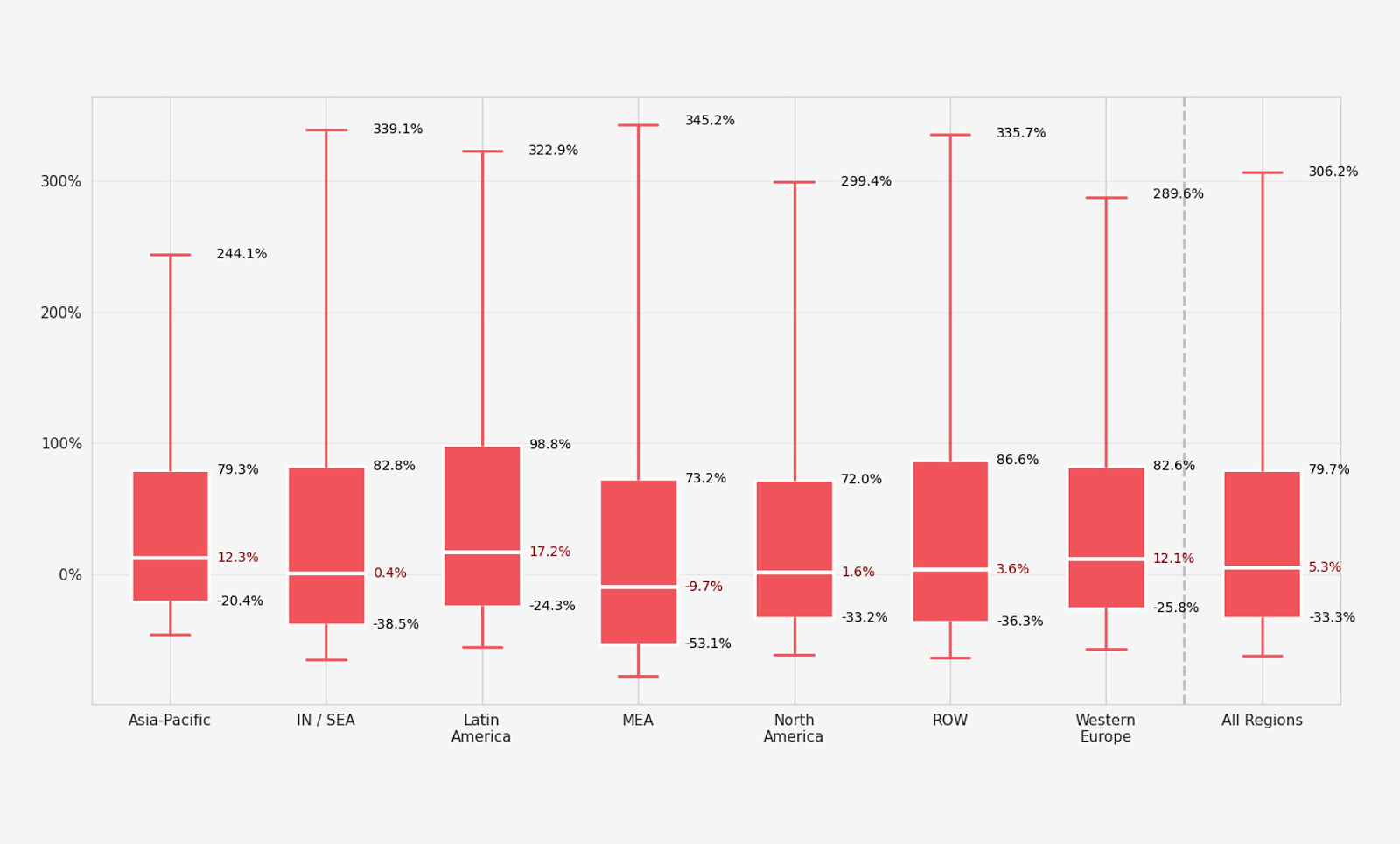

2026 shows a huge polarization in app growth. Where maintaining steady growth (e.g. 5–15% YoY) was previously considered safe and healthy for an app business, today’s data shows this middle ground evaporating beneath our feet.

Market dynamics — user acquisition costs, algorithm changes, platform fees, AI unit economics — now heavily reward the top performers, creating a mobile app economy that mirrors broader wealth inequality: the rich get richer, and indie developers struggle to stay afloat.

The data:

- Top quartile: the top 25% of subscription apps grew their monthly recurring revenue (MRR) by 80% or more year-on-year

- Bottom quartile: the bottom 25% of apps saw their MRR shrink by more than 33%

- The divide: this creates a massive 113-point gap between the winners scaling aggressively and the apps bleeding revenue

- Comparison to 2025: last year’s data saw the revenue gap increase between the top 5% and bottom 25% (with the top earning 400x more, up from 200x in 2024) – a trend the 2026 data confirms and quantifies for the first time in growth rate

Median year-on-year monthly recurring revenue growth rate, by developer HQ — State of Subscription Apps 2026

What next?

App teams can no longer rest on ‘good enough’. There is no safety blanket. If you’re growing at the median rate (5–17%), you’re at risk of falling into the bottom quartile and slipping through the cracks. Teams need to shift from maintenance mode to aggressive growth optimization.

→ Your next step: learn about the Subscription Value Loop, a framework for app growth

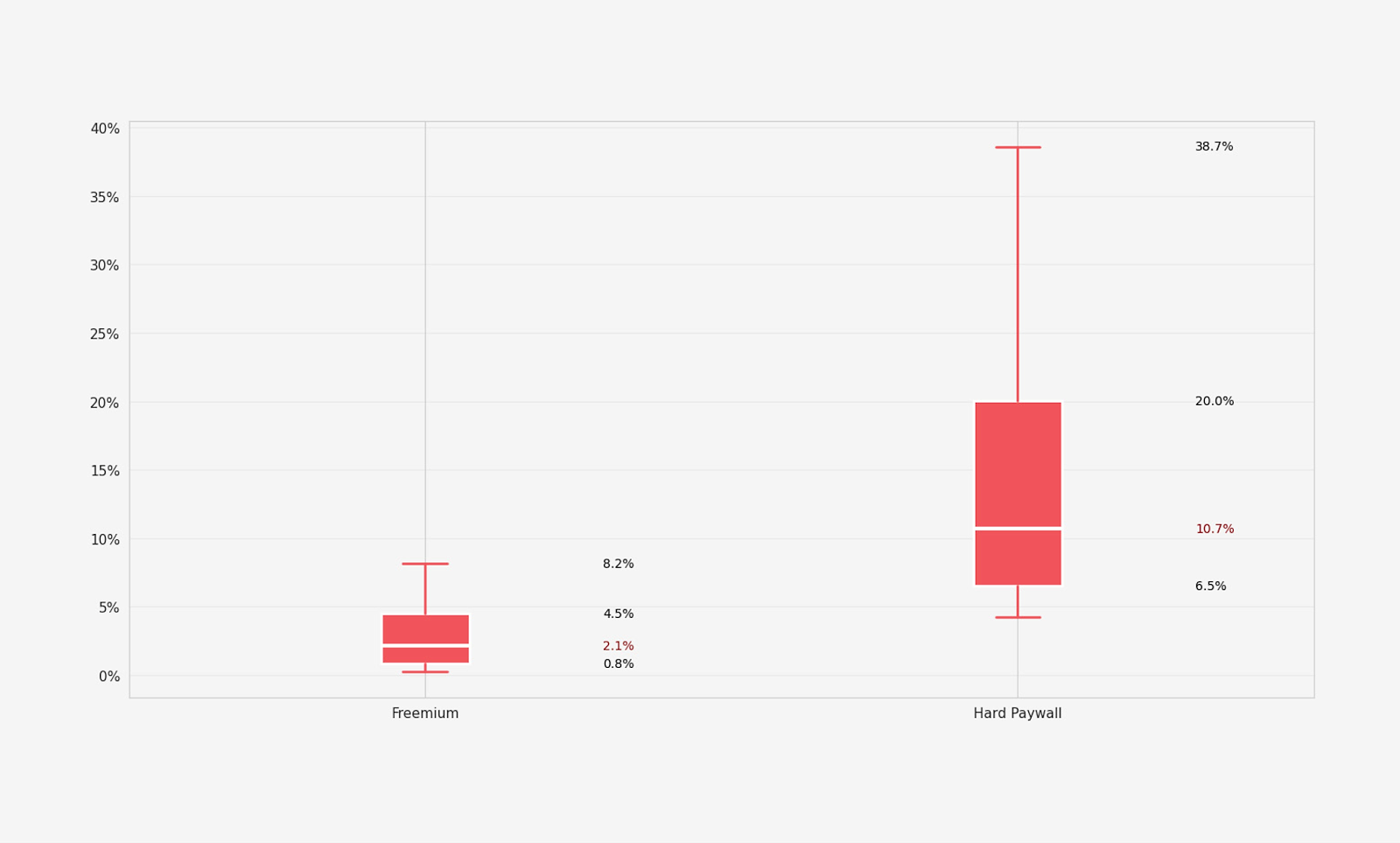

2. Hard paywalls convert 5x better than freemium

We’ve all heard the rhetoric that “hard paywalls kill user experience”. Well, consider that mythbusted. Across categories, Day 35 trial-to-paid conversion is 5x better when apps feature a hard paywall. Contrary to popular belief, hard paywalls are not scaring users away or ‘forcing’ them into buying before ready — this narrative only belittles users, who are subscription-savvy and will only convert when they want to. Today, users are engaging with hard paywalls, and it’s giving apps faster payback.

This choice [hard paywall vs. freemium] changes your unit economics completely. Same ad spend. Dramatically different revenue on day one. — Sven Jürgens, Mobile Growth Consultant

While paywall type impacts conversion, long-term retention equalizes across both access methods. Freemium apps continue to convert well into Week 6 and beyond, meaning the full conversion picture is a longer game than you may think.

So freemium doesn’t mean less success — and there are many successful freemium apps that prove this — but the data definitively proves that hard paywalls convert better, and convert quicker. In 2026, freemium may feel like the safer option, but it’s not necessarily the best choice.

The data:

- Conversion: hard paywalls have a median Day-35 trial-to-paid conversion rate of 10.7%, compared to just 2.1% for freemium apps — this is roughly a 5x advantage

- Retention: freemium apps retain 28% of yearly subscribers after 1 year, while hard paywall apps retain 27%, making the difference statistically negligible

- Revenue per install: hard paywall apps generate 8x higher RPI at day 60, compared to freemium ($3.09 vs. $0.38)

- Comparison to 2025: while freemium D35 conversion has remained at 2.1% since 2025, hard paywall conversion has gone down ~2% (12.1% in 2025), suggesting a broader reluctance to convert

Day 35 download-to-paid, freemium vs. hard paywall — State of Subscription Apps 2026

What next?

Switch to a hard paywall (if you dare 😈). Hard paywalls offer an upfront ROI, giving you a chunk of cash to reinvest in growth. If you’re relying on a freemium model to build goodwill, you’re sacrificing massive top-of-funnel revenue for a just 1% retention bump a year later. Given the aggressive market, it’s a risky move to take.

→ Your next step: discover what the best subscription apps get right about paywalls

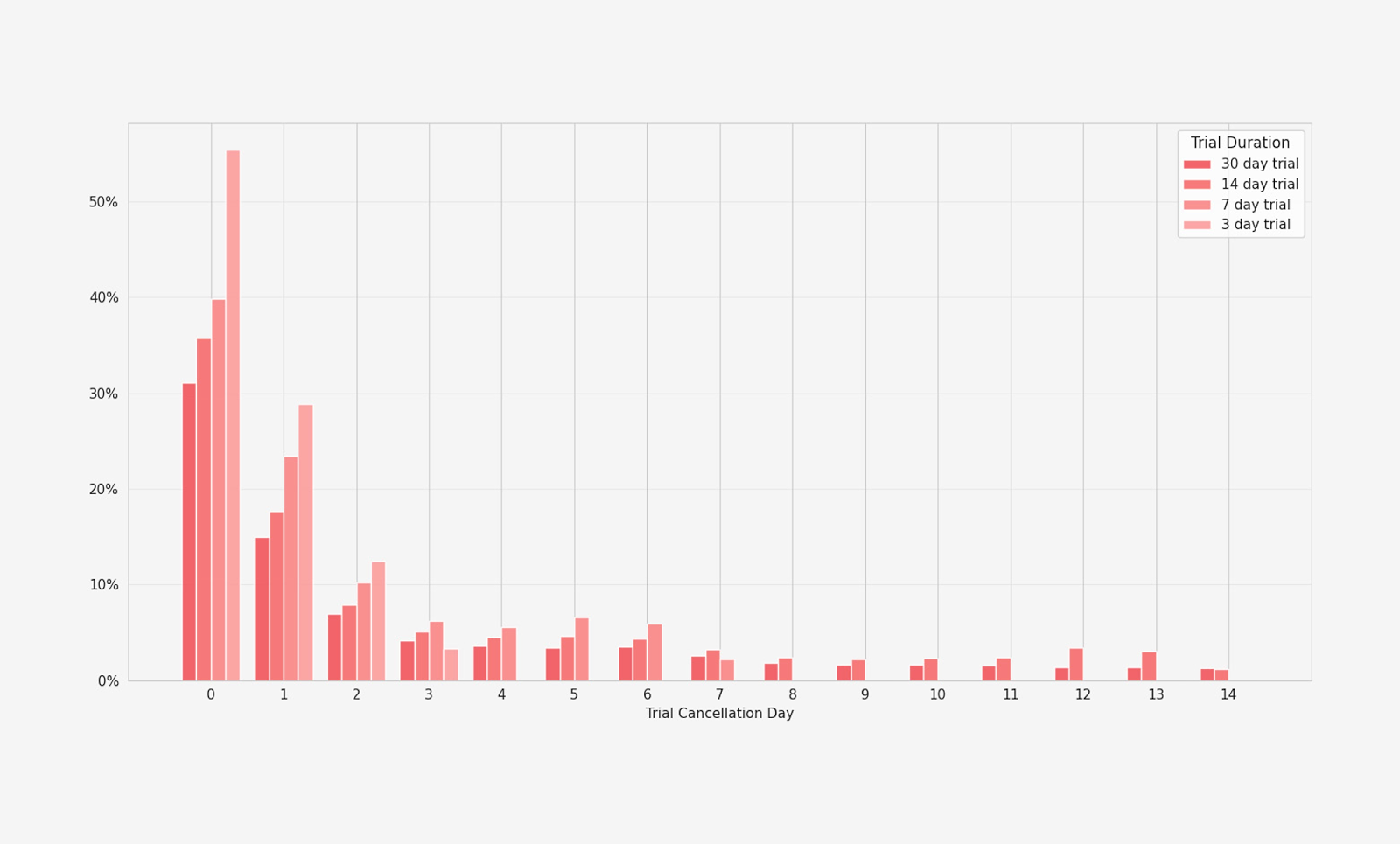

3. The Day 0 buyer’s remorse window

Plot twist: your 3-day trial is actually a 1-hour trial. Yep. 55% of all trial cancellations happen on Day 0. So while developers are designing a three-day experience, the modern consumer’s attention span is demanding instant proof of value.

Teams can no longer assume users spend days exploring all app features before making a decision; the reality is that users treat app trials like impulsive retail purchases. They subscribe to get past the paywall, immediately experience and assess the core features, then cancel to prevent being charged. If you don’t deliver an aha! moment in the first 60 minutes, the subscriber is already gone.

The data:

- Day 0 cancellations: exactly 55.4% of all 3-day trial cancellations occur on Day 0

- The drop-off: an overwhelming 84% of 3-day trial cancellations happen between Day 0 and Day 1

- Comparison to 2025: last year, ~51% of 3-day trial cancellations happened on Day 0 (showing a ~4% increase this year), suggesting users quickfire cancel instinct is only increasing

% of trial cancellations, by day and trial duration — State of Subscription Apps 2026

What next?

Treat your onboarding flow as your primary retention mechanism. If a user doesn’t hit the aha! moment in their very first session, they’re going to quickly toggle off auto-renew. Revisit your trial length — does it need to be three days? (More on this next.)) Consider the features you give access to in a trial — what shows value instantly, and what takes up space? Figure out the most direct route to proving value, then build it.

→ Your next step: stop chasing growth hacks — learn how how to fix your onboarding first

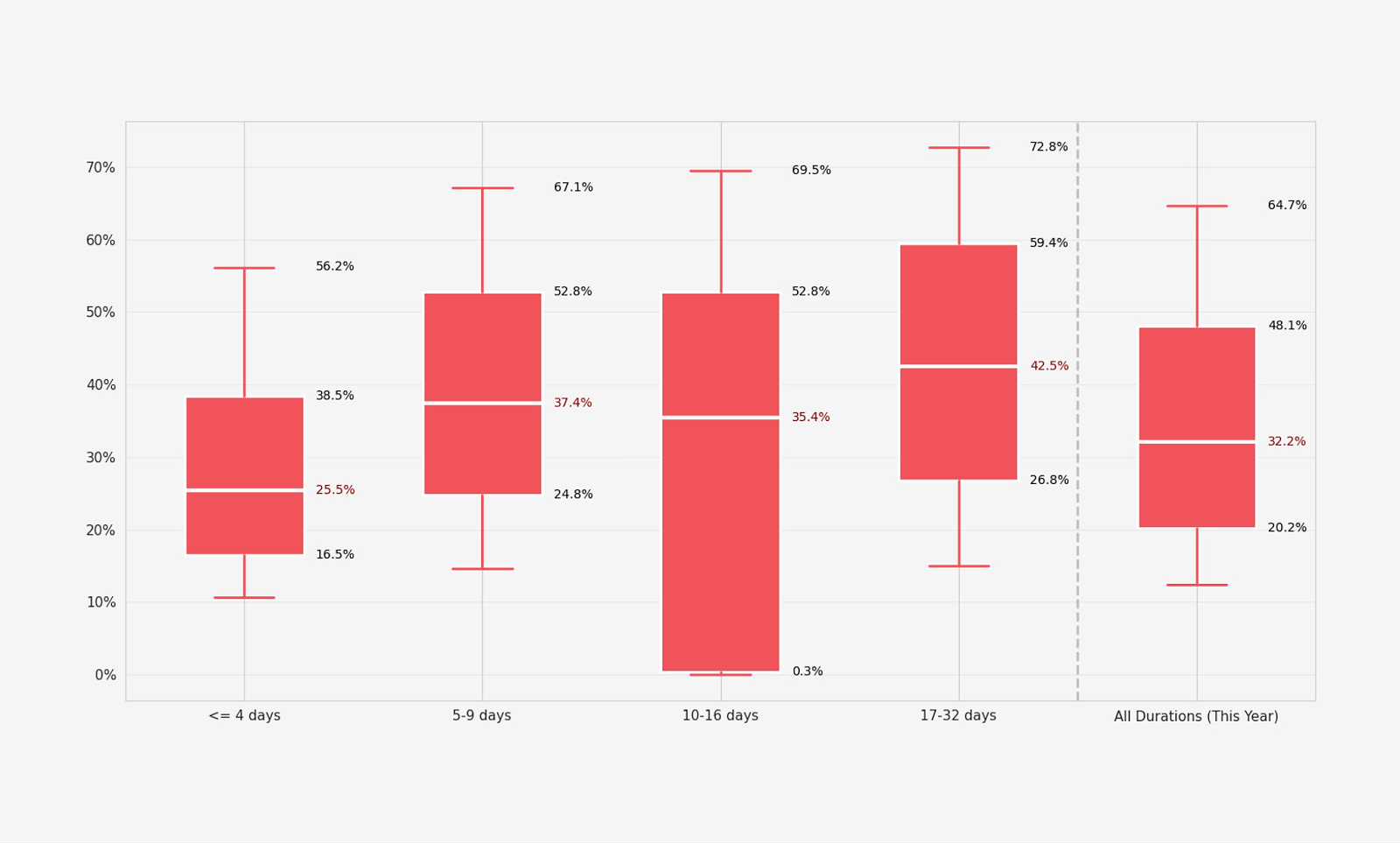

4. The 7 day trial is alive and kicking (sometimes)

The subscription app industry is obsessed with short trials, but what do the numbers actually show? Is the 7-day trial really dead?

In short, no.

Trials of 17-32 days convert 70% better than 3-day trials (42.5% vs 25.5%). Yet, 46% of apps are moving to trials of 4 days or less. Why? Growth teams are under market and economic pressure to show fast revenue.

Most developers do 3-day free trials for cashflow. You want the money in three days, not 30 days. [Or you’re looking to] get conversion data faster, to compound onboarding and paywall experiments. — David Barnard and Jacob Eiting speak about on Sub Club

Short trials force a fast decision from users, often resulting in high abandonment (see the Day 0 cancellation rate of 3-day trial vs. longer), while longer trials give users time to integrate an app into their daily habits, and reduces nerves about accidental auto-renewal. 3-day trials are useful for app teams, but the reality is you’re sacrificing long-term conversion for a short-term dopamine dashboard spike.

The data:

- Long-trial conversion: trials of 17–32 days convert at an incredibly high median of 42.5%

- Short trial conversion: trials of <4 days convert at just 25.5%, meaning long trials convert ~70% better

- Comparison to 2025: last year, trials were increasing in length, but today, despite the data, trials of <4 days rose from 42.1% in 2025 to 46.5% in 2026

Trial-to-paid, by trial duration — State of Subscription Apps 2026

What next?

Deep dive into your category’s trial and retention data. Watch the crowd, but don’t feel locked in to follow them. Try experimenting with longer trial length and see how your conversion and retention changes. Show value upfront, then give users adequate time to experience it.

→ Your next step: determine the optimum trial length for your app

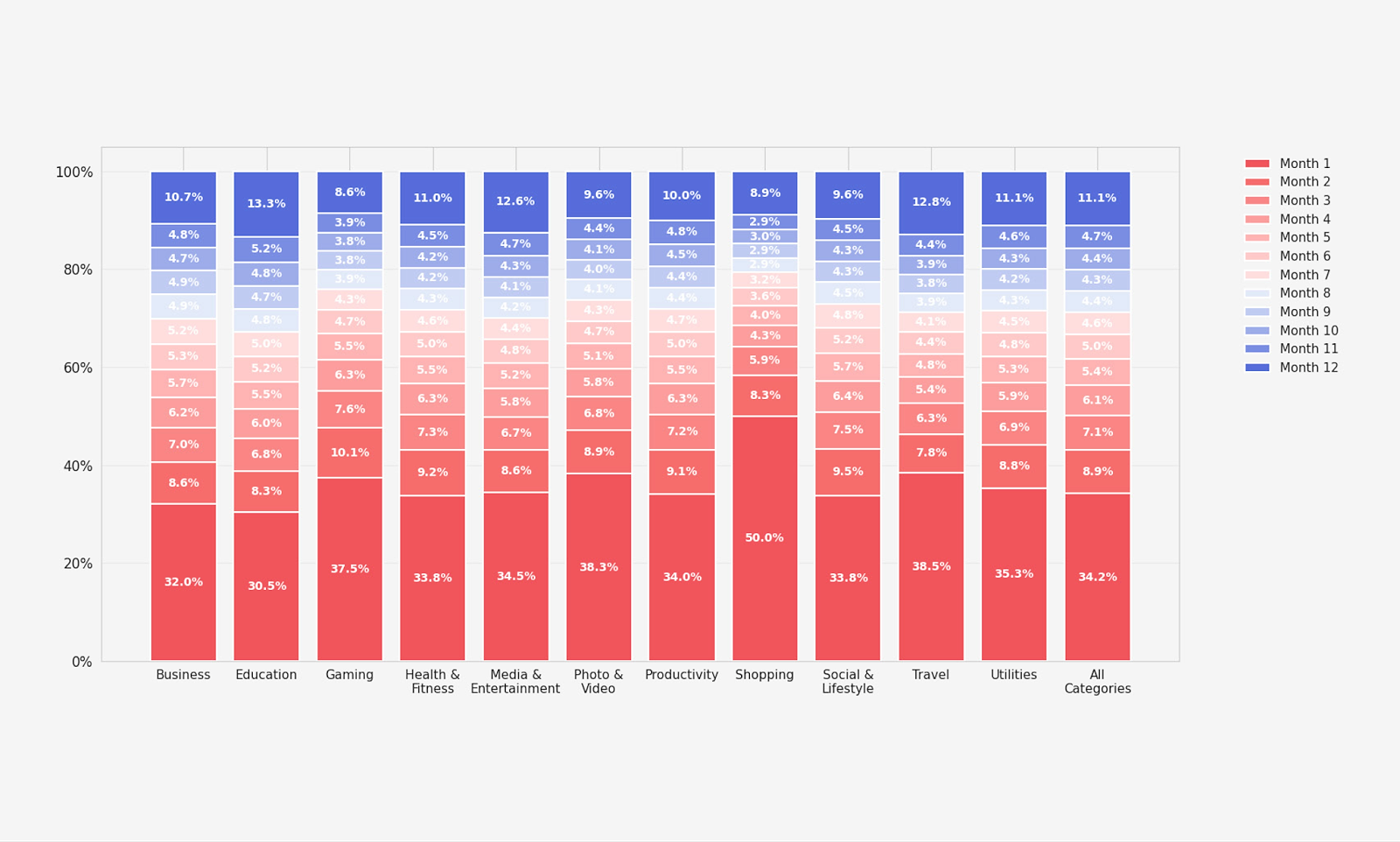

5. Annual subscriptions aren’t the guarantee you think they are

When users buy an annual subscription, it feels like a sigh of relief for the developer. You relax, assuming that annual sub means 12 months to prove the app’s value. 12 months to demonstrate each carefully-designed feature, and deliver a clear message of “I should keep using this app” come Year 2.

But the data reveals a harsh truth: over one third of users cancel auto-renewal within the first month. Users aren’t stupid, and they don’t think of an annual subscription as a rolling purchase — they consider it a one-off payment for this year, then immediately protect their wallet. Meaning that Year 2 revenue you’d already relied on? It’s gone before Year 1 has even really begun.

The data:

- Month 1 churn: the first month accounts for 35% of all annual cancellations

- The cancellation curve: after the Month 1 spike, cancellations drop to just 3–10% for the middle of the year, before spiking again in Month 12 (pre-renewal)

- Comparison to 2025: ~56% of annual subscribers cancelled in Year 1 in 2025, while this worsened to ~72% in 2026; however the Month 1 cancellation spike remains fairly comparable between years

Cancellation timeline for annual subscriptions — State of Subscription Apps 2026

What next?

App teams can no longer rely on users ‘forgetting’ about an annual subscription. The battle for Year 2 starts in Week 1. You don’t have 11 months to win an annual renewal, you need to preemptively convince users to not cancel auto-renew. This means intensive value reinforcement from the moment they download, and win-back campaigns throughout the first two months to persuade users to toggle auto-renew back on, while they’re first engaged.

→ Your next step: explore the pros and cons of annual subscriptions, then learn how to improve your annual subscription uptake

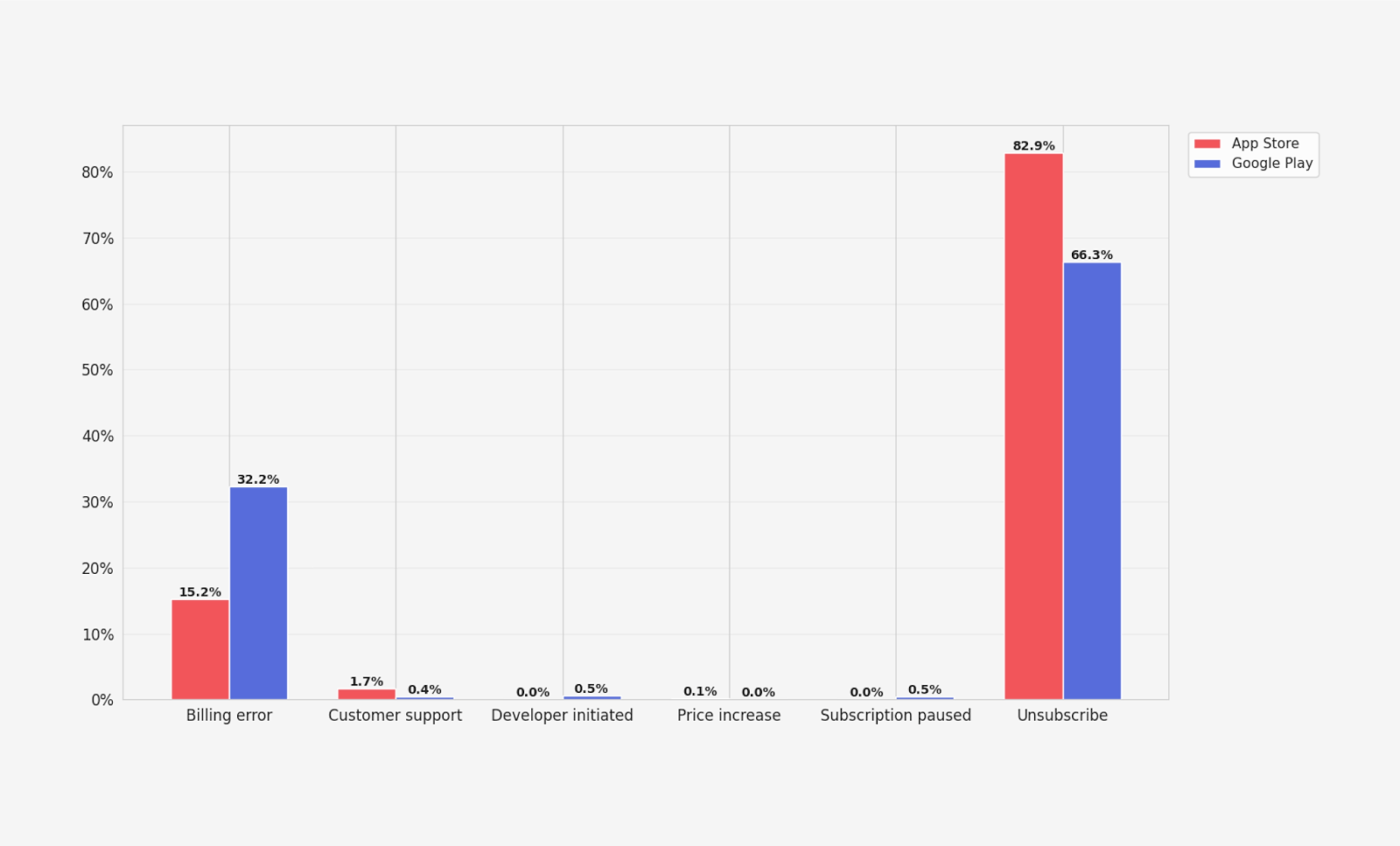

6. The Google Play tax

For Android devs, growth is actually an engineering problem. 31% of Google Play cancellations are involuntary billing failures — over double the rate of the App Store (14%).

When an app loses a subscriber, blame usually falls to the product features or pricing. However, for Android apps, nearly a third of churn isn’t because the user hated the app, it’s simply because their credit card failed, expired, or was declined, and the app’s billing infrastructure wasn’t robust enough to recover it.

This money is unclaimed revenue: growth isn’t just about ads; it’s about plugging the technical leaks in Google Play’s ecosystem through better retry logic and grace periods.

The data:

- Google Play billing failures: a massive 31% of all subscription cancellations on Google Play are due to billing errors

- App Store comparison: on the App Store, billing errors account for only 14% of cancellations

- Comparison to 2025: Google Play’s billing errors have worsened, from 28.2% in 2025 to 31% this year; meanwhile the App Store’s improved, reducing billing errors by 1.1% (15.1% in 2025 vs. 14% in 2026)

Cancellation reasons, by app store — State of Subscription Apps 2026

What next?

If you have a significant Android user base, your highest ROI activity is optimizing your dunning process (billing retries) and enabling grace periods. Handled appropriately, Android apps can almost instantly recover 15-20% of lost revenue, without acquiring a single new user.

→ Your next step: learn how to counteract the Google Play billing leak, and set up winback campaigns for lapsed subscribers

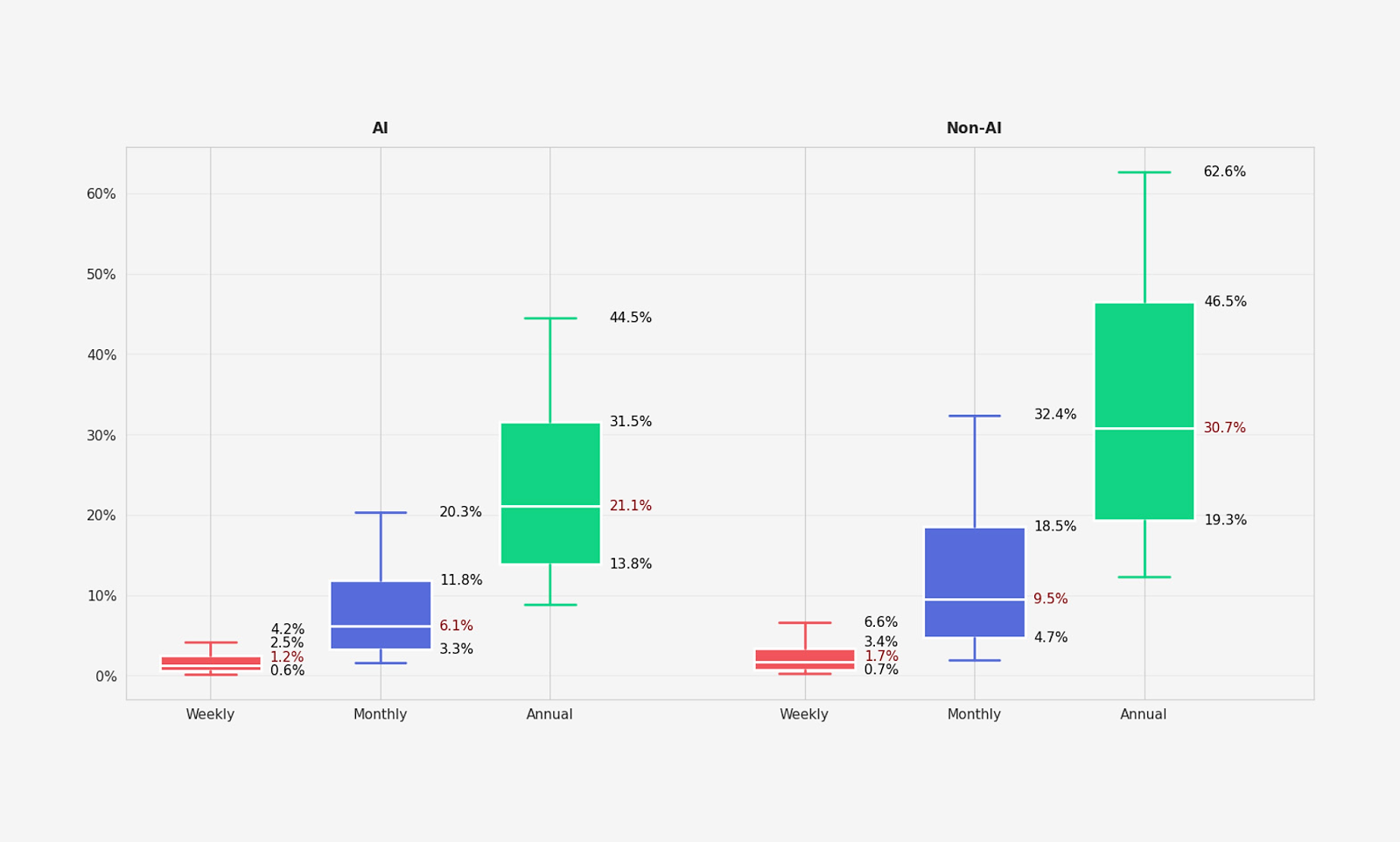

7. The AI paradox: acquisition beast, retention nightmare

AI sells like crazy, but it doesn’t stick. While AI-powered apps generate 41% more revenue-per-user, those same apps churn 36% faster than non-AI apps. The problem isn’t convincing users to download your AI app (clearly, users want to pay for AI), the challenge is keeping them invested.

Amidst the vibe coding hype and established developers watching as new apps dilute market real estate, the data proves AI apps aren’t in it for the long haul (yet). AI features are driving massive trial revenue, yet many AI apps suffer from an alarming lack of product-market fit. Users may be willing to pay a premium to try AI tools, but once they download, they’re not finding the long-term utility to justify its hefty pricetag.

Yes, vibe coded apps can ship fast. Yes, AI features act as a massive top-of-funnel magnet, but this doesn’t guarantee the same audience further down the line. It doesn’t mean they can sustain a user base. Experienced developers still have an edge: stamina. They know how to maintain an app, build trust with an audience, and grow revenue. That is the real differentiator between what apps succeed and which fall behind — not who can build an app fastest, what AI features it has, or whether a human or agent wrote the lines of code.

The data:

- The AI premium: AI apps sustain a 41% Year 1 realized LTV premium compared to non-AI apps ($30.16 median vs. $21.37 median)

- The churn problem: Despite the high revenue, AI monthly plans retain 36% worse over 12 months than traditional apps

- Comparison to 2025: AI apps showed 12-month payer retention of 9.2% (App Store) and 11.5% (Google Play), comparable to traditional apps in respective categories; suggesting 2026’s sharp dip in retention is a problem emerging after AI apps settled into mainstream and users had longer to assess them

Retained subscribers after 12 months, by AI vs. non-AI — State of Subscription Apps 2026

What next?

Shipping fast or relying on AI hype isn’t enough. If you add AI to your app, use the influx of cash to build a genuine user experience and robust backend. Don’t rely on novelty or one-off AI gimmicks. These will only churn in a few months. Look to established apps for retention and growth lessons, then use AI to make them happen fast. The long game will be won not by AI vs. non-AI, but by whoever can utilize AI and human expertise.

→ Your next step: revisit core value offered to users and secure product-market fit

Looking to 2027

The data from 2026’s State of Subscription Apps report highlights emerging shifts in the app industry, from the influx of new apps (14,000+ a month!) to the rapid dissolving of the average app’s revenue safety net. But many of these trends are not surprising — Google’s billing leak has been a prominent issue for several years, and the relationship between trial length and conversion isn’t new either. What is clear from 2026’s data is that apps can no longer afford to ignore these accumulating changes and known issues.

‘Good enough’ is no longer good enough. Just as quickly as top apps are growing their revenue, the lower quartile are churning it. Subscription apps that are designed with user value as the core and marketed with intention have found their place in the ecosystem. Their success compounds over time, and the rest of the app store is left fighting over scraps. All that’s left is for teams to decide which side of the line they wish to sit on come 2027’s report.